What pensions do teachers want?

Report

Publication

Executive summary

For the past decade, governments have wrestled with too many teachers leaving the profession, and too few joining. This government has promised to reverse that by recruiting an additional 6,500 expert teachers but, as yet, there is no clear plan to achieve it. Perhaps the only policy mechanism strong enough is pay, yet teachers’ pay has fallen 14 per cent behind that of the wider economy since 2010. Meaningful pay rises for teachers are the obvious solution but they are expensive. With the chancellor committed to fiscal restraint and budgets already stretched, education leaders are left searching for ways to improve teachers’ compensation without incurring additional costs.

One possible approach to improving teachers’ compensation is to provide teachers with greater flexibility over balance between pension contributions and salary, so they can choose the compensation package that best meets their needs. However, that would require changes to the way teachers’ pensions are provided. This report outlines the current pension landscape for teachers in England, and presents new findings from a survey of teachers on the scale of demand for changes, and which aspects of pensions teachers care most about.

Teachers’ pensions are generous but inflexible

- All teachers in state-funded schools are automatically enrolled in the Teachers’ Pension Scheme (TPS). It is a defined benefit scheme with pension benefits based on average earnings over a teacher’s career. Being a defined benefit scheme, the level of retirement income is guaranteed.

- Teachers contributions depend on their salary with average contribution rates of 9.6 per cent. It is not flexible and teachers cannot choose their contribution rate.

- Schools’ contributions have risen over the past fifteen years to 28.6 per cent, for a total contribution rate of 38.6 per cent of a teacher’s salary. Schools also cannot choose or vary their contribution rate.

- Teachers must have at least two years of service to qualify for the TPS and, if they opt out, there is typically no alternative scheme available to them.

- In contrast, the minimum employer contribution to an employee’s auto-enrolled, defined contribution pension is 8 per cent, and modelling suggests that a total contribution rate of 12 per cent over a lifetime will usually be sufficient to ensure a satisfactory retirement income. However, that adequacy depends upon the pension pot’s investment returns and is not guaranteed. These schemes typically allow employees to vary their contribution rate as they please.

What do teachers want?

We conducted a survey in collaboration with Teacher Tapp, to reveal teachers’ preferred compensation packages and understand the balance of salary and pension contributions. The survey presented 5,750 teachers with a series of choices between different compensation packages, varying in current salary, retirement income, and the certainty of their retirement income. We found:

- Salary today matters more than retirement income: Teachers value a 10 per cent increase in retirement income as much as a 6.3 per cent increase in salary, meaning that salary increases are 1.6 times as valuable as pension increases.

- Loss aversion: Decreases in teachers’ income hurt twice as much as gains in income help. Teachers were 21 percentage points less likely to choose a compensation package with a 10 per cent salary cut, but only 9.1 percentage points more likely to choose a compensation package with the same salary increase.

- Preference for guaranteed retirement income: Teachers showed a strong preference for guaranteed retirement income over income dependent on stock market performance. Losing the guaranteed retirement income of a defined benefit scheme, like the TPS, is as bad for the average teacher’s wellbeing as a 10 per cent salary cut.

- Some teachers have a stronger preference for salary increases over pensions: Younger teachers, and those with lower financial security, care more about their immediate salary. Salary changes affect the wellbeing of teachers in their twenties about twice as much as they affect teachers in their fifties. The effect is similar for teachers struggling to make ends meet, though less pronounced.

One in seven teachers would prefer a different pension arrangement

- Despite teachers valuing losses twice as much as gains, about 15 per cent of teachers prefer a 10 per cent increase in salary to the status quo, even if it means switching to a defined contribution pension and accepting a 20 per cent lower retirement income.

- Teachers in their twenties are two-thirds more likely to make this trade-off than teachers in their fifties. We found that 19 per cent of teachers in their twenties would make this trade-off, compared to only 11 per cent of teachers in their fifties.

- It is possible that new entrants to teaching may be even more likely to make this trade-off because they do not face the same loss aversion as teachers who are already enrolled in the TPS. A more attractive salary offer could help recruitment to the profession, as well as retention.

Recommendations

- Continue to permit schools to offer multiple pension plans: A substantial minority of teachers clearly prefer to trade some retirement income for current salary, which is not currently possible within the TPS. Schools should be allowed to continue to offer alternative arrangements to their staff, alongside the TPS.

- Investigate the possibility of providing flexibility within TPS: The government should consider reviewing the TPS with recruitment and retention in mind. It may be that, as with schemes such as the civil service’s, there is room to offer more flexibility within the TPS.

- Conduct research on policy options: Research should be conducted into the likely impact and consequences of various policy options, with the goal of offering a set of schemes that promote recruitment and retention, while still ensuring retirement security for teachers.

Introduction

The teaching profession in England is facing significant challenges in recruitment and retention. Schools are struggling to attract and retain qualified teachers, with a third of teachers leaving the profession within the first five years of their careers.1 This threatens the quality of education and the stability of the teaching workforce and has been exacerbated by falling teacher pay, which has declined by 14 per cent in real terms since 2010.2 Compounding these challenges are the fiscal constraints faced by the government: the Chancellor has emphasised the need for fiscal prudence, which has limited the scope for substantial pay rises for teachers. For 2025, the Department for Education (DfE) has recommended a pay rise of just 2.8 per cent for teachers.3

The government has committed to recruiting an additional 6,500 expert teachers in this Parliament but that will be extremely difficult if teachers’ pay is not returned to parity with comparable occupations. However, pay is not the only element of teachers’ remuneration: public sector pensions are typically far more generous than in the private sector and form a significant part of a teacher’s remuneration package. In 2020, the Office for National Statistics estimated that public sector pay lagged the private sector by 3 per cent, but total remuneration in the public sector was 7 per cent greater than in the private sector due to the difference in pensions.4 Pay rises are needed but that does not mean the existing expenditure could not be more effectively deployed.

Unfortunately, despite the generosity of teachers’ pensions, the overall compensation package is not always as attractive as it could be. Public sector pension schemes are often less flexible than private sector workplace pensions, which makes it harder to match the compensation package to employees’ needs. The most recent National Audit Office review of public sector pensions found that the inflexibility of the schemes posed risks to recruitment and retention, particularly among younger staff who might value higher pay in exchange for a lower pension entitlement.5

Public sector managers have realised the limitations of the existing schemes and are slowly beginning to take action. First, the Civil Service Pension Scheme introduced an alternative scheme in 2002, which mirrors the flexibility of many private sector pensions.6 Then, in 2019, the Department of Health and Social Care conducted a well-received consultation on slightly increasing the flexibility of NHS pensions.7 Finally, in 2024, United Learning, a large multi-academy trust, proposed to offered their staff the option to switch to a more flexible workplace pension scheme, which would allow them to exchange some of their pension contribution for additional salary.8 Unlike in the NHS consultation - which was for a far less radical change - teachers’ unions have been strongly opposed to the proposal, claiming that it undermines traditional teachers’ pensions.9

Last year, EPI worked with Teacher Tapp to immediately survey teachers in England and ask them whether they would be interested in such a scheme. Over 40 per cent of all teachers, and nearly 60 per cent of teachers in their twenties, said they might be interested, in principle, in exchanging some pension for salary (Figure 1).10

That survey showed teachers’ interest but did not explore how much they would be willing to trade, on what terms, and how much a trade might be worth to them. In this follow-up work, we have conducted a more detailed survey to answer those questions. This report outlines the current pension landscape for teachers in England, the potential changes, and which aspects of pensions teachers care most about.

The landscape of teachers’ pensions in England

The Teachers’ Pension Scheme (TPS) is a cornerstone of the compensation package for teachers in England, providing a defined benefit pension that guarantees a specific income in retirement. It is a public sector pension scheme, backed by the government, and offers generous benefits, many of which are unavailable in typical workplace pensions. As of 2025, all serving teachers are now auto-enrolled for the career average section of the TPS, where they build up 1/57 of their pensionable earnings as pension each year. These pension rights are then increased annually until retirement at the rate of inflation plus 1.6 per cent for teachers who remain in teaching.11

The TPS contrasts with typical workplace pension schemes offered in the private sector, which are usually defined contribution (DC) schemes. In these schemes, the employee and employer contribute to a pension pot, which is then usually invested by the scheme. The employee uses the pot in retirement to buy an annuity or draw down income. The level of retirement income is not guaranteed and depends on the performance of the pension pot’s investments.

In common with most public sector pension schemes, the TPS is an ‘unfunded’ scheme, which means that the benefits are paid out of the contributions of current members rather than from a dedicated fund. That means today’s teachers are paying for the pensions of today’s retirees, and their pensions will be paid for by the next generation of teachers. Any difference is made up by HM Treasury. Increased contributions today will not necessarily lead to increased benefits for today’s teachers but, typically, reflect increases in the cost of paying the guaranteed benefits to today’s retirees.

Teachers’ contributions to the TPS are based on their salary and vary between 7.4 and 11.7 per cent of salary, depending on how much the teacher earns. Schools contribute an additional 28.6 per cent, for a total contribution rate of 38.2 per cent of a teacher’s salary.12 Neither teachers, nor schools, can choose their contribution rate, and it is not possible to vary the rate of contribution based on individual circumstances or preferences.

This contrasts with a DC pension where the employee can choose their contribution rate, within certain limits, and vary it as they please. The trade-off with the DC pension is that the level of retirement income is not guaranteed and depends on the amount contributed and the performance of the pension pot’s investments. In our survey, we investigated how much teachers value the certainty of a DB pension.

Impact of increased TPS contribution rates on schools

Schools’ required employer contribution to the TPS has increased significantly over the past fifteen years, from 14.1 per cent in 2012 to 28.6 per cent in 2024, reflecting the rising cost of providing guaranteed pension benefits to teachers. This has placed a significant financial burden on schools, particularly independent schools, which do not receive government funding to cover the increased contributions.13 For state-funded schools, the government committed to funding the increased contributions for the 2024/25 financial year but that is still money that could have been used elsewhere in the Department for Education’s budget.

The cost of the increased contributions is most obvious among independent schools, which do not receive government funding for the increases. The financial impact of the increased contribution rates has led many independent schools to explore alternative pension arrangements. Since 2019, nearly 580 independent schools have notified the Department for Education of their intention to withdraw from the TPS due to affordability concerns. As of mid-2024, 34 per cent of all independent schools in England and Wales have either withdrawn or plan to withdraw from the TPS.14 Some schools have opted for phased withdrawal, where current staff remain in the TPS, but new staff are enrolled in alternative pension schemes.15 Others have withdrawn from the TPS entirely and moved their staff across to DC schemes that are, typically, less generous.

One notable example of innovation in response to the TPS changes is United Learning, one of the largest multi-academy trusts in the UK. In July 2024 it announced that it would be providing teachers at its state-funded schools with the flexibility to opt out of the TPS and receive some of the pension contribution the trust would otherwise have made as salary.16 The trust’s chief executive, Sir Jon Coles, said that the scheme would allow teachers to increase their take-home pay by up to 24 per cent while maintaining a 10 per cent pension contribution to a DC pension scheme. He pointed out that 10 per cent of the trust’s staff already opt out of the TPS to save themselves the employee contribution, which leaves them with no pension provision. The new scheme would allow them to take that money as salary instead, while still providing them with a pension through the employer contribution.

An important difference between this scheme and many of the schemes in independent schools, is that it is not proposed as a cost-saving measure for the school. The scheme is cost-neutral for the school and merely affects the balance between pension contributions and salary, whereas most schemes in independent schools also reduce teachers’ overall compensation. The aim is to improve recruitment to the trust’s schools by providing teachers with the option of taking more of their compensation as salary. This is the type of flexibility we are interested in examining in this study.

Previous research

Teachers’ pensions have not always been a topic of intense interest in England, but there has been considerable research done in the US, particularly in the context of public sector compensation and retirement planning.

Evidence from the US

A significant body of research has focused on teachers’ willingness to pay for various retirement benefits. Fuchsman, McGee, and Zamarro (2020) conducted a nationally representative survey using a discrete choice experiment (DCE) to estimate teachers’ willingness to pay for different retirement plan characteristics. Their findings indicate that teachers are generally indifferent between traditional DB pensions and alternative retirement plans if the alternatives are paired with a 2-3 per cent salary increase.17 This suggests that salary adjustments can compensate for changes in retirement plan design, making alternative plans more acceptable to teachers. They also found that more experienced teachers have a stronger preference for traditional DB pensions compared to their less experienced counterparts.

Johnston (2021) explored the broader compensation preferences of teachers, including salary, performance pay, and retirement benefits. His research shows that schools tend to overpay in retirement benefits while underpaying in salary, relative to teachers’ preferences. This misalignment indicates potential gains from restructuring compensation to better match teachers’ preferences and improve retention.18

The choice between different types of pension plans is influenced by various factors, including investment risk and individual preferences. A study by Koedel and Podgursky (2016) analysed the determinants of teachers’ choices between traditional DB plans and hybrid plans, which combine elements of DB and DC plans. Their findings suggest that teachers’ risk aversion plays a significant role in their pension plan choices, with risk-averse teachers preferring the stability of DB plans.19

Finally, Biasi (2024) examined the relative effectiveness of salaries and pensions in retaining public-sector employees, using data from Wisconsin teachers. Her research found that teachers respond more strongly to changes in salaries than to changes in pensions of the same size. This suggests that while pensions are important, salaries may be a more effective tool for attracting and retaining teachers, especially in times of fiscal constraint.20

Evidence from England

Burge, Lu, and Phillips (2021) conducted a comprehensive study using DCEs to measure teacher retention in England. Commissioned by the UK Office of Manpower Economics, this study involved over 2,200 teachers and aimed to understand the trade-offs teachers are willing to make between pay, rewards, and other working conditions. On pensions, it found that teachers are highly loss averse and value losses almost three times as highly as gains. A 1 per cent increase in final pension was valued at only 0.55 per cent of current pay, but a 1 per cent loss in final pension would require a 1.67 per cent increase in salary to compensate..21 This loss aversion is typical in the literature and is important to account for in our experimental design.

A survey of teachers in England

Building on that work, EPI collaborated with Teacher Tapp to run a survey of teachers in England that asked them how much they value the main elements of their compensation. The survey implemented a DCE, which is a method that presents teachers with a series of choices between two compensation packages, varying in current salary, retirement income, and the certainty of retirement income. Teachers were asked to choose the package they preferred in each set of choices, allowing us to estimate the relative importance of each attribute. For details of the method, see the appendix.

Survey design

The survey was conducted on December 4, 2024 via Teacher Tapp, which surveys teachers in England daily. We had 5,705 usable responses from teachers, which were broadly representative of teachers in England. The appendix also provides more details on the sample demographics.

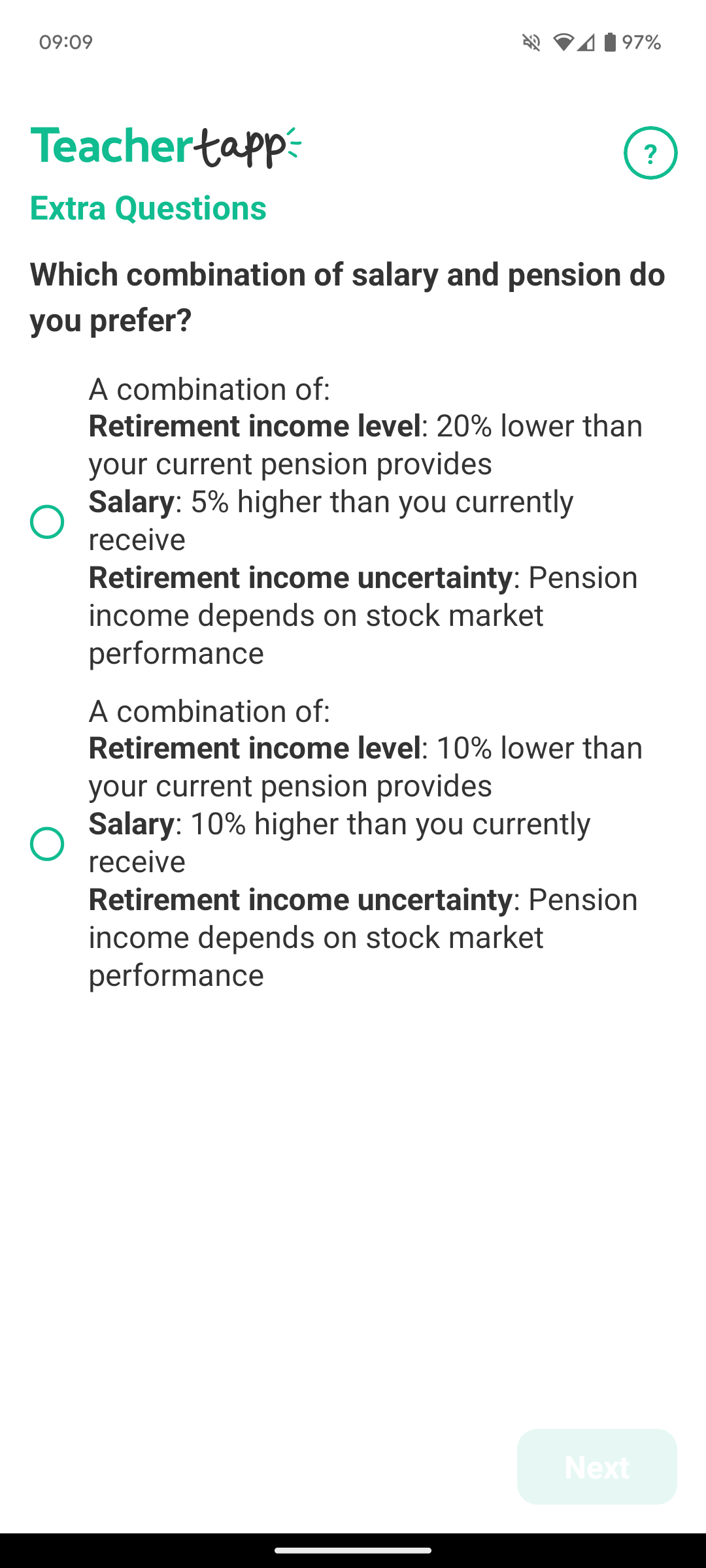

The survey presented teachers with a series of choices between two different compensation packages. Each teacher saw five sets of choices, and each set contained two options. The options varied based on three main attributes:

- Current Salary: This could be 10 per cent less, 5 per cent less, the same, 5 per cent more, or 10 per cent more than the teacher’s current salary.

- Retirement Income: This could be 20 per cent less, 10 per cent less, the same, 10 per cent more, or 20 per cent more than the teacher’s current pension.

- Certainty of Retirement Income: This could either be guaranteed (like a traditional pension) or dependent on stock market performance (like a defined contribution plan).

Teachers were asked to choose the option they preferred in each set. The survey also collected information about the teachers’ demographics, including their age, current salary, current pension scheme, career intentions, and financial security.

We then used a statistical model to estimate the impact of each attribute on the probability of choosing a compensation package.

Interpreting the results

The results of the model are presented in two ways:

- Average marginal component effects (AMCEs): These represent the average change in the probability of choosing a compensation package associated with a one-unit change in the attribute level. For example, an AMCE of 0.05 for a 10 per cent higher salary means that a 10 per cent increase in salary increases the probability of choosing that compensation package by 5 percentage points. We show these effects with 95 per cent confidence intervals in each chart below.

- Preference shares: These represent the proportion of teachers who prefer a compensation package with a specific set of attributes. For example, a preference share of 0.9 for a 5 per cent higher salary, relative to the status quo means that 90 per cent of teachers prefer a package with a 5 per cent higher salary. These probabilities are not quite the same as the proportion of teachers who would choose the package in a real-world scenario, because they do not account for all the other options teachers have, nor for the fact that teachers might be unaware of the full range of options available to them.

Survey results

Which pension scheme do teachers currently have?

The default pension scheme for teachers in England is the TPS. However, some teachers may have opted out of the TPS and have a pension scheme with another employer or, if they are teaching at a private school, their school may no longer offer it as an option. Figure 2 shows the distribution of pension schemes by school type.

It shows that the vast majority of teachers in state-funded schools are in the TPS, with only 0.7% of teachers at state-funded schools in an alternative pension scheme. In contrast, teachers in private schools are more likely to have such a pension scheme, with 43.1% reporting that they are in an alternative employer pension scheme.

We also find that only 1.4% of teachers in state-funded schools and 1.4% of teachers in private schools do not have a pension. That contrasts with United Learning’s experience, where 10 per cent of staff opt out of the TPS.

| Pension scheme | State-funded school | Independent school |

|---|---|---|

| Teachers’ Pension Scheme (TPS) | 96.4% (5,267) | 55.1% (239) |

| Another employer pension scheme | 0.7% (38) | 43.1% (187) |

| I don’t know | 1.6% (86) | 0.5% (2) |

| Not currently enrolled in an employer pension scheme | 1.4% (74) | 1.4% (6) |

What do teachers value about their compensation?

Here we present the results of the discrete choice experiment. The results show how teachers value different attributes of their compensation package and how they trade off between salary, pension, and pension type.

Figure 3 below shows the AMCEs of the pension attributes on the probability of choosing an option. Each point on the chart shows the change in probability of choosing a compensation package if it has the specified attribute, rather than the status quo. For example, it shows that having a salary 10 per cent higher makes the average teacher about 9 percentage points more likely to choose a compensation package, relative to salary remaining the same. Similarly, the prospect of a DC pension makes a teacher about 22 percentage points less likely to choose a compensation package, relative to having a DB pension, when all other attributes are held constant.

Four things are immediately apparent from Figure 3:

- Teachers prefer higher incomes, both today and in retirement.

- Teachers prefer money today over money in the future.

- Teachers prefer certainty over their retirement income.

- Teachers exhibit loss aversion.

Salary and retirement income

Teachers, unsurprisingly, have a strong preference for more income, both today and in the future. They are 9 per cent more likely to choose a compensation package with a 10 per cent higher salary, and 5.6 per cent more likely to choose a compensation package with 10 per cent more retirement income.

However, as those figures show, they do not value salary today as high as retirement income. The respondents valued a 1 per cent increase in retirement income as much as a 0.62 per cent increase in salary, meaning that salary increases are 1.6 times as valuable as pension increases.

This finding is consistent with the only other similar experiment to address this question with teachers in England. Burge, Lu, and Phillips22 found that a “1 per cent increase in final pension was valued equivalent to a 0.5 per cent increase in annual pay”.

The value of certainty

In general, people prefer certainty and are willing to pay a premium for it. They will accept a lower expected income if it is guaranteed. In the context of pensions, a defined benefit scheme, like the TPS, guarantees a certain level of income in retirement. A defined contribution scheme, on the other hand, depends on the performance of the pension scheme’s assets, which fluctuates.

Figure 3 shows that teachers are 22 percentage points less likely to switch to a compensation package that depends on the stock market compared to one that guarantees their final retirement income. To put it in context, this is equivalent to a teacher being willing to accept a 10 per cent lower salary to ensure their retirement income is guaranteed, which is considerably more than was found in a similar US study.23

It is worth noting that the phrasing of this attribute referred to ‘stock market performance’. In reality, schemes are likely to invest in a blend of equities, bonds, and other assets, and the performance of the scheme will depend on the mix of assets. The phrasing was chosen to be simple and clear to respondents but it is possible that respondents were reacting to the specifics of a relatively risky asset class.

Loss aversion

Finally, teachers value losses more than twice as much as gains. This phenomenon is known as loss aversion and means that cutting a benefit is more painful than increasing it is pleasurable. Teachers were 22 percentage points less likely to choose a compensation package with a 10 per cent salary cut, but only 9 percentage points more likely to choose a compensation package with a 10 per cent salary increase.

Similarly, a 10 per cent increase in retirement income made a teacher 5.6 per cent more likely to choose a compensation package, but they are 12 per cent less likely to choose a compensation package with a 10 per cent cut. Despite the differences between gains and losses, the trade-off between salary and pension is very similar across both.

Differences by teacher characteristics

The analysis above shows the average effect of the pension attributes on the probability of choosing an option. However, teachers are a diverse group, and their preferences may vary based on their individual characteristics. To explore this, we can estimate the differences in the AMCEs between groups.

Drawing on our previous analysis, we examined the following teacher characteristics:24

- School funding: state-funded school or private school.

- Age.

- Salary.

- Current pension scheme: TPS or another scheme.

- Career intentions: how long teachers expect to stay in the profession.

- Financial security: how well teachers feel they are managing financially.

We did not find any significant differences in the AMCEs by salary or career intentions. However, we did find significant differences by age, school funding, and financial security. There are also differences by current pension scheme, but these are confounded by the fact that teachers in private schools are more likely to have a defined contribution pension scheme, so we cannot examine them separately without a larger sample.

School funding

Teachers in private schools are already far more likely to have a defined contribution pension scheme than those in state schools, who are typically in the TPS. Figure 2, above, showed that, in our sample, 43% of teachers in private schools have a defined contribution scheme, compared to only 0.7% of teachers in state schools.

Despite that, Figure 4 shows that teachers in private schools are equally as averse to DC pensions as teachers in state schools. They also appear to care slightly more about salary than teachers in state schools, and to perhaps have slightly less loss aversion. However, the differences are not precisely estimated due to the small number of teachers in private schools in our sample.

Age

In our earlier analysis, young teachers were far more likely to say they’d be willing to trade pension for salary, which is consistent with overseas findings.25 This analysis also shows that, the younger a teacher is, the more sensitive they are to salary and the less valuable they find their pension (Figure 5). Teachers in their twenties are also slightly less averse to having a DC pension than teachers in their fifties.

Financial security

Teachers who are more financially secure are generally less sensitive to salary increases and more sensitive to pension increases.

Simulating policy changes

One of the key findings from the analysis is that teachers value salary more than pension. This suggests that some teachers would be willing to accept a lower pension in exchange for a higher salary. To understand how many would like to switch, we can simulate a policy change where teachers are offered a choice between a compensation package with a higher salary and a lower pension, and their current compensation package, and estimate how many teachers would switch.26

To estimate the impact of a scheme like United Learning’s, where teachers take a salary increase in exchange for a cut in pension contributions in a DC scheme, we need to include the change in retirement income. In reality, that depends on the teacher’s current assets, accrued pension benefits, household earnings, and their time until retirement. We cannot account for each teacher’s circumstances but pension calculators indicate a permanent 10 percentage point reduction in pension contributions could lead to roughly a 20 per cent reduction in retirement income for an individual with moderate savings. This will not hold for all teachers but it is sufficient to illustrate the choice teachers are making.

The simulation we run is to compare teachers’ choices across two compensation packages:

| Attribute | Option 1: TPS | Option 2: DC alternative |

|---|---|---|

| Salary | Same | 10 per cent higher |

| Pension | Same | 20 per cent lower |

| Pension type | Defined benefit | Defined contribution |

The results of the simulation (Figure 8) indicate that younger teachers are more likely to switch to the new compensation package, with teachers in their 20s being the most likely to switch. However, even among young teachers, only a minority would choose the new compensation package, largely because they value the defined benefit pension highly.

The same is true of teachers who are experiencing financial insecurity. Teachers who are financially struggling are a quarter more likely to want to trade pension entitlement for salary than teachers who are financially comfortably. Teachers who are financially secure are less likely to switch, but still a substantial minority would choose the new compensation package.

Policy implications

Consequences of the findings

The findings from the DCE provide several lessons for teachers’ compensation. First, most teachers place a high value on their defined benefit pension with guaranteed retirement income. Unions have been strong advocates for the TPS and the findings suggest that this matches the preferences of most teachers. The forced move to DC schemes, as implemented by many independent schools, would need to be compensated by at least a 10 per cent salary increase to compensate teachers. That is implausible with the current funding constraints, so it is essential to maintain the TPS as an option for teachers.

A substantial minority of teachers, particularly younger teachers and those with financial insecurity, would like to trade some pension for salary. This suggests that offering flexibility could be attractive to some teachers and keep them in the profession. Not all teachers have the same preferences and plans, and the inflexibility of the TPS means it may not be the best option for all teachers. Finding a way to offer a mix of defined benefit and defined contribution schemes could allow the minority of teachers who would like to trade pension for salary to do so, while maintaining the TPS for those who value it.

Teachers are strongly loss averse, meaning that they value losses more than gains. That means there may be compensation packages that are very attractive to some people but which they would not switch to if they were receiving a different package. That has implications for the recruitment of people to the teaching profession, who are not yet receiving any compensation. Giving them the option at the point of entry to the profession may allow them to better match the compensation package to their preferences, without experiencing the loss associated with being placed in one package by default and then having to switch.

The survey captured only the preferences of current teachers who, by definition, have chosen to stay in the profession. It is possible that the preferences of those who have left are different. It is also possible that the preferences of those who have not yet entered the profession are different. Providing flexibility around compensation may be a way to attract and retain teachers whose preferences are not currently being met by the inflexibility of the TPS.

Potential impact of policy changes

The goal of any changes around pension provision should be to attract and retain high-quality teachers. These findings indicate that there are a substantial minority of teachers who would like to trade some pension for salary, particularly younger teachers and those with financial insecurity. Previous work has indicated that increasing pay for early-career teachers has an elasticity of exits with respect to salary of about 3.27 That implies a 10 per cent increase in pay might reduce attrition by about 30 per cent.

Nearly 40,000 teachers quit teaching in 2022/23 and our simulation suggests about 15 per cent of teachers might be interested in switching to a higher salary. If that reduced the attrition of that group by 30 per cent (assuming an elasticity of 3), that might keep an additional 1,800 teachers in the profession each year. However, that is likely an upper bound because the teachers who consider switching may not be representative of all teachers and may respond differently to incentives. The estimates of the elasticity are also based on uncompensated salary increases, rather than financial flexibility, so the true elasticity for this policy is very likely to be lower. Further research is required to understand the potential impacts of policies on the teaching workforce.

Research is also required into the design and implementation of any flexibility. Financial planning is complex and poor choices can have serious repercussions for teachers’ financial security in retirement. The option to reduce pension contributions in exchange for a higher salary may be attractive when a teacher is trying to save the deposit for a house, or struggling to make ends meet. However, persistent under-saving for retirement can have serious consequences, and current regulations around auto-enrolled pensions may be insufficient to ensure a comfortable retirement. Which? and the Pensions Policy Institute’s estimate that the current auto-enrolment minimum contribution rate of 8 per cent is likely to be inadequate for many people to maintain their standard of living in retirement. The minimum total contribution to an employee’s auto-enrolled, defined contribution pension is 8 per cent, and modelling suggests that a total contribution rate of 12 per cent over a lifetime will usually be sufficient to ensure a satisfactory retirement income.28 Teachers need to be aware of the trade-offs they are making and the consequences of those choices, and default options and advice need to be in place to help teachers make the best choices for their circumstances.

Recommendations

Allow pension flexibility

Recommendation: Continue to permit schools to offer multiple pension plans to their staff.

Rationale: A substantial minority of teachers clearly prefer to trade some retirement income for current salary, which is not currently possible within the TPS. Schools should be allowed to continue to offer alternative arrangements to their staff, alongside the TPS.

Investigate the possibility of providing flexibility within TPS

Recommendation: Investigate the possibility of providing flexibility within TPS to allow teachers to switch between defined benefit (DB) and defined contribution (DC) schemes.

Rationale: The government should consider reviewing the TPS with recruitment and retention in mind. It may be that, as with schemes such as the civil service’s, there is room to offer more flexibility within the TPS.

Conduct research on policy options

Recommendation: Research should be conducted into the likely impact and consequences of various policy options, with the goal of offering a set of schemes that promote recruitment and retention, while still ensuring retirement security for teachers.

Rationale: There are many types of pension scheme and methods of implementation that could allow the flexibility desired by some teachers. However, it is important that the approaches chosen are those most likely to improve recruitment and retention of excellent teachers. At present, it is unclear what impact flexibility might have on teachers’ career choices. It is also essential that teachers have a secure retirement after spending a career in schools, and the structure of their pension scheme should not jeopardise that. Research is needed into the structure of schemes and their implications for the trade-off between income during their retirement and their working lives.

Appendix: Methods

Survey

The survey implemented a discrete choice experiment where each teacher was presented with 5 choice sets. Each choice set presented two compensation options and teachers were asked to choose the option they preferred. The options varied on three attributes, which had the following possible levels:

- The current salary

- 10 per cent less than the teacher’s current salary.

- 5 per cent less than the teacher’s current salary.

- The teacher’s current salary.

- 5 per cent more than the teacher’s current salary.

- 10 per cent more than the teacher’s current salary.

- The retirement income

- 20 per cent less than the teacher’s current pension provides.

- 10 per cent less than the teacher’s current pension provides.

- The same as the teacher’s current pension.

- 10 per cent more than the teacher’s current pension provides.

- 20 per cent more than the teacher’s current pension provides.

- The certainty of the retirement income

- Pension guarantees final retirement income.

- Pension income depends on stock market performance.

Attributes were randomly assigned to each option in each choice set.

An example of how a respondent would see a choice set on the Teacher Tapp app is shown below in Figure 10.

The survey also collected information on respondents’ demographics, and on four other relevant attributes. Response options are shown in Figure 11:

The teacher’s current pension scheme.

The teacher’s current salary.

Whether the teacher expected to be a teacher in three years time (ie career intentions).

Whether the teacher’s household earns enough to live on and save (ie financial security). Response options for this attribute are abbreviated in Figure 11. The options shown to teachers were:

- Yes, comfortably (e.g. we are able to take a holiday abroad each year)

- Yes, reasonably comfortably (e.g. our salaries cover our bills and expenses each month with a little left over)

- No, we are scraping by (e.g. sometimes we cannot cover our monthly bills and expenses)

- No, our income falls well short of how much we need to run our household

- Would prefer not to say

Additionally, the options for ‘scraping by’ and ‘well short’ were combined into a single category of ‘struggling’ for the analysis because the sample size for ‘well short’ was too small to be useful.

The survey was conducted on 4 December 2024 through Teacher Tapp and received responses from 5,929 teachers.

Discrete choice analysis

Discrete choice experiments are built on a random utility function, which assume that the utility a teacher derives from a particular compensation package can be decomposed into a systematic component and a random component. Let \(U_{ij}\) represent the utility that teacher \(i\) derives from choosing compensation package \(j\). This utility can be expressed as:

\[ U_{ij} = V_{ij} + \epsilon_{ij} \]

where:

\(V_{ij}\) is the systematic component of the utility, which is a function of the observed attributes of the compensation package. \(\epsilon_{ij}\) is the random component of the utility, capturing unobserved factors and assumed to be independently and identically distributed (i.i.d.) with a Type I Extreme Value distribution.

The systematic component of the utility, \(V_{ij}\), is modelled as a linear function of the attributes of the compensation package:

\[ V_{ij} = \beta_1 \text{Salary}_{ij} + \beta_2 \text{RetirementIncome}_{ij} + \beta_3 \text{PensionType}_{ij} \]

where:

- \(\text{Salary}_{ij}\) represents the salary level of option \(j\) for teacher \(i\).

- \(\text{RetirementIncome}_{ij}\) represents the retirement income level of option \(j\) for teacher \(i\).

- \(\text{PensionType}_{ij}\) represents the certainty of the retirement income of option \(j\) for teacher \(i\).

- $_1, _2, \(\beta_3\) are the coefficients to be estimated, representing the importance of each attribute.

The probability that teacher \(i\) chooses compensation package \(j\) over another package \(k\) is given by the logistic choice probability:

\[ P_{ij} = \frac{\exp(V_{ij})}{\exp(V_{ij}) + \exp(V_{ik})} \]

where \(V_{ij}\) and \(V_{ik}\) are the systematic utilities of the two options in the choice set.

The parameters \(\beta_1\), \(\beta_2\), \(\beta_3\) are estimated using a logistic regression model, where the dependent variable is the binary choice indicator (1 if the option is chosen, 0 otherwise), and the independent variables are the attributes of the compensation packages. This setup allows us to quantify the impact of each attribute on the probability of choosing a compensation package, providing insights into teachers’ preferences for different aspects of their compensation.

The model we estimate is:

\[ \text{logit}(P_{ij}) = \beta_1 \text{Salary}_{ij} + \beta_2 \text{RetirementIncome}_{ij} + \beta_3 \text{PensionType}_{ij} \]

Estimation is performed using a survey-weighted logistic regression model in the R package survey. The survey weights are used to ensure that the results are representative of the population of teachers in England. Standard errors are adjusted for clustering at the respondent level.

We do not model question set effects because each question set is equally randomized and no different from the others.

AMCEs split by demographics are modelled as interactions between the demographic variable and the choice attributes.

Data

Data cleaning

The data were provided by Teacher Tapp with some initial cleaning and exclusions already performed. They reported to EPI that there were 7,437 teachers who responded to at least one of the questions in the survey. Of those, 6,658 answered all five rounds, and 5,929 gave a valid phase (either primary or secondary), seniority (classroom teacher, middle leader, SLT excl head, or headteacher), and country (ie they teach in England).

That brings the total number of survey respondents in the dataset provided to EPI to 5,705, which is the dataset described below. All respondents have 10 records associated with them, one for each of two options in each of five choice sets they were presented with.

For the analysis, we have excluded respondents who answered “Not relevant / cannot answer” to any of the demographic questions we rely upon, or who did not answer them at all. Those key demographic questions relate to:

- School type

- Age

- Salary

- Financial security

- Career intentions

Doing that drops 2,240 responses, which accounts for 224 of our 5,929 respondents, and leaves us with 57,050 responses for our discrete choice analysis from 5,705 respondents.

Descriptive statistics

Figure 11 displays unweighted descriptive statistics for the key demographic variables in the sample at respondent level.

| Characteristic | N = 5,9291 |

|---|---|

| demog_age | |

| Age in 20s | 602 (10%) |

| Age in 30s | 1,876 (32%) |

| Age in 40s | 2,051 (35%) |

| Age in 50s+ | 1,391 (23%) |

| Unknown | 9 |

| demog_gender | |

| Female | 4,406 (75%) |

| Male | 1,489 (25%) |

| Unknown | 34 |

| demog_experience | |

| Less than 5 years | 730 (12%) |

| Between 5 and 10 years | 1,194 (20%) |

| Between 10 and 20 years | 2,204 (37%) |

| Over 20 years | 1,770 (30%) |

| Unknown | 31 |

| demog_funding | |

| State-funded school | 5,480 (93%) |

| Private School | 434 (7.3%) |

| Unknown | 15 |

| demog_phase | |

| Primary | 2,054 (35%) |

| Secondary | 3,875 (65%) |

| demog_seniority | |

| Headteacher | 352 (5.9%) |

| SLT (excl head) | 1,194 (20%) |

| Middle Leader | 2,419 (41%) |

| Classroom Teacher | 1,964 (33%) |

| demog_region | |

| North West | 653 (11%) |

| Yorkshire and North East | 723 (12%) |

| East of England | 781 (13%) |

| Midlands | 1,051 (18%) |

| South West | 659 (11%) |

| London | 735 (12%) |

| South East | 1,327 (22%) |

| demog_subject | |

| Science | 839 (18%) |

| KS2 | 1,150 (25%) |

| Maths | 668 (14%) |

| Humanities | 734 (16%) |

| English | 678 (15%) |

| EYFS/KS1 | 541 (12%) |

| Unknown | 1,319 |

| demog_children | |

| No children at home | 2,681 (46%) |

| Under 5 | 808 (14%) |

| 5-11 years | 969 (16%) |

| Over 11 years | 1,424 (24%) |

| Unknown | 47 |

| demog_financial | |

| Comfortable | 2,061 (35%) |

| Reasonable | 2,954 (50%) |

| Scraping by | 767 (13%) |

| Falling short | 75 (1.3%) |

| Prefer not to say | 51 (0.9%) |

| Not relevant / cannot answer | 20 (0.3%) |

| Unknown | 1 |

| demog_pension | |

| Teachers' Pension Scheme (TPS) | 5,519 (93%) |

| Another employer pension scheme | 226 (3.8%) |

| I don't know | 88 (1.5%) |

| Not currently enrolled in an employer pension scheme | 80 (1.4%) |

| Not relevant / cannot answer | 3 (<0.1%) |

| Unknown | 13 |

| demog_stay_in_teaching | |

| Yes, most likely | 3,506 (59%) |

| Perhaps | 1,519 (26%) |

| No, probably not | 742 (13%) |

| Don't know | 133 (2.2%) |

| Not relevant / cannot answer | 16 (0.3%) |

| Unknown | 13 |

| demog_salary | |

| less than £24,000 | 96 (1.6%) |

| £24,000 to £34,999 | 695 (12%) |

| £35,000 to £44,999 | 1,338 (23%) |

| £45,000 to £54,999 | 1,838 (31%) |

| £55,000 to £64,999 | 929 (16%) |

| £65,000 to £74,999 | 460 (7.8%) |

| £75,000 to £84,999 | 189 (3.2%) |

| £85,000 to £94,999 | 67 (1.1%) |

| £95,000 to £104,999 | 42 (0.7%) |

| £105,000 or more | 39 (0.7%) |

| Not relevant / cannot answer | 23 (0.4%) |

| I don't want to say | 212 (3.6%) |

| Unknown | 1 |

| demog_financial_binned | |

| Comfortable | 2,061 (35%) |

| Reasonable | 2,954 (50%) |

| Struggling | 842 (14%) |

| Not relevant / cannot answer | 20 (0.3%) |

| Unknown | 52 |

| 1 n (%) | |

Sample demographics

Comparison of the demographics of the analysis sample with the population of teachers in England (Figure 12).

Inattention

Inattention in a discrete choice experiment can lead to biased estimates if teachers are not paying attention to the survey. We check for several specific forms of inattention.

Time taken to complete the survey

The survey recorded the time taken to complete the survey in milliseconds. The median time taken to complete the survey was 81 seconds. Figure 13 below shows the distribution of time taken to complete the survey.

To check whether this is biasing the results, we can re-estimate the core results after dropping the quickest and slowest 2.5 per cent of responses, which retains responses ranging from 19 to 573 seconds in duration.

Dominated responses

Inattention can also be detected by looking at the distribution of responses to the choice sets. If teachers are not paying attention, we would expect the responses to be either random or to follow a pattern where they always choose the same option.

Random responses are hard to detect because they can be indistinguishable from true preferences. However, we can look for choice sets where a teacher chooses a strictly dominated option. A strictly dominated option is one where there is another option that is better in every respect. If a teacher chooses a strictly dominated option, it suggests that they are not paying attention.

Figure 14 below shows the number of dominated options chosen by respondents.

| Number of dominated options chosen (of 5 total) | Number of respondents |

|---|---|

| 0 | 4471 |

| 1 | 928 |

| 2 | 249 |

| 3 | 52 |

| 4 | 5 |

With 1,602 dominated options chosen by respondents, it is possible that inattention is a significant issue in this survey.

Straightlining

Straightlining is a form of inattention where respondents always choose the same option. We can check for straightlining by looking at the distribution of responses to the choice sets. If teachers are straightlining, we would expect the responses to follow a pattern where they always choose the same option.

Figure 15 below shows the number of respondents who always chose the same option.

| Always chose the same option | Number of respondents | Proportion of respondents |

|---|---|---|

| FALSE | 5041 | 88.36% |

| TRUE | 664 | 11.64% |

If respondents chose randomly, we would expect the proportion of respondents who always chose the same option to be around 1 in 32, or 3.1%. If respondents are straightlining, we would expect this proportion to be higher, which it is, at 11.6%. That suggests straightlining may be affecting up to 664 respondents, though it is also possible they have legitimately chosen those options.

Comparison of inattention results

For each of the three types of inattention, we have re-estimated the core results using only the unaffected responses. The results in Figure 16 show that the core results are robust to inattention. The estimates of the coefficients are similar across all models, suggesting that inattention is not a significant issue in this survey.

| Characteristic |

Core

|

Time taken

|

Dominated

|

Straightlining

|

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| N | log(OR)1 | SE | N | log(OR)1 | SE | N | log(OR)1 | SE | N | log(OR)1 | SE | |

| choice_salary | 57,017 | 53,949 | 55,383 | 50,361 | ||||||||

| Same | — | — | — | — | — | — | — | — | ||||

| 10% lower | -1.0*** | 0.036 | -1.1*** | 0.037 | -1.1*** | 0.037 | -1.1*** | 0.038 | ||||

| 5% lower | -0.49*** | 0.034 | -0.52*** | 0.035 | -0.54*** | 0.035 | -0.52*** | 0.036 | ||||

| 5% higher | 0.13*** | 0.034 | 0.14*** | 0.035 | 0.16*** | 0.035 | 0.14*** | 0.036 | ||||

| 10% higher | 0.42*** | 0.035 | 0.43*** | 0.036 | 0.50*** | 0.036 | 0.45*** | 0.037 | ||||

| choice_pension | 57,017 | 53,949 | 55,383 | 50,361 | ||||||||

| Same | — | — | — | — | — | — | — | — | ||||

| 20% lower | -1.1*** | 0.037 | -1.2*** | 0.038 | -1.3*** | 0.038 | -1.2*** | 0.039 | ||||

| 10% lower | -0.55*** | 0.034 | -0.57*** | 0.035 | -0.58*** | 0.036 | -0.59*** | 0.037 | ||||

| 10% higher | 0.26*** | 0.035 | 0.27*** | 0.036 | 0.30*** | 0.036 | 0.27*** | 0.037 | ||||

| 20% higher | 0.50*** | 0.034 | 0.52*** | 0.035 | 0.58*** | 0.035 | 0.53*** | 0.037 | ||||

| choice_pensiontype | 57,017 | 53,949 | 55,383 | 50,361 | ||||||||

| Defined benefit | — | — | — | — | — | — | — | — | ||||

| Defined contribution | -1.0*** | 0.025 | -1.0*** | 0.025 | -1.1*** | 0.025 | -1.1*** | 0.026 | ||||

| Abbreviations: CI = Confidence Interval, OR = Odds Ratio, SE = Standard Error | ||||||||||||

| 1 *p<0.05; **p<0.01; ***p<0.001 | ||||||||||||

References

Barton, Neil. “Latest Update – Independent Schools Leaving the Teachers’ Pension Scheme.” Broadstone, April 2021.

Biasi, Barbara. “Salaries, Pensions, and the Retention of Public-Sector Employees: Evidence from Wisconsin Teachers.” Working Paper. New Haven, July 2024.

Burge, Peter, Hui Lu, and William Phillips. “Understanding Teaching Retention: Using a Discrete Choice Experiment to Measure Teacher Retention in England,” February 2021.

Chapman, Chris, and Elea McDonnell Feit. R For Marketing Research and Analytics. Use R! Cham: Springer International Publishing, 2019. https://doi.org/10.1007/978-3-030-14316-9.

Chiripanhura, Blessing. “Public and Private Sector Earnings.” Office for National Statistics, September 2020.

Coles, Jon. “Why We’re Reforming Our Pension Offer.” Schools Week, July 2024.

Cumiskey, Lucas. “Unions Lobby Phillipson over United Learning Pension Plans,” July 2024.

Department for Education. “Evidence to the STRB: 2025 Pay Award for Teachers and Leaders.” UK: Department for Education, December 2024.

Fuchsman, Dillon, Josh B. McGee, and Gema Zamarro. “Teachers’ Willingness To Pay For Retirement Benefits: A National Stated Preferences Experiment.” EdWorkingPapers.com. Annenberg Institute at Brown University, October 2020.

Hutchinson, Jo, Joni Kelly, Luke Sibieta, and James Zuccollo. “Incentives to Recruit and Retain Teachers in Wales.” London: Education Policy Institute, November 2024.

Johnston, Andrew C., and Jonah Rockoff. “Pension Reform and Labor Supply.” EdWorkingPapers.com. Annenberg Institute at Brown University, May 2022.

Koedel, Cory, and Michael Podgursky. “Teacher Pension Systems, the Composition of the Teaching Workforce, and Teacher Quality. Working Paper 72.” National Center for Analysis of Longitudinal Data in Education Research, 2012.

McLean, Dawson, Jack Worth, and Andrew Smith. “Teacher Labour Market in England: Annual Report 2024.” NFER, 2024.

National Audit Office. “Public Service Pensions.” Report -- {{Value}} for Money. London: National Audit Office, March 2021.

“Partnership Pension Account.” Civil Service Pension Scheme. https://www.civilservicepensionscheme.org.uk/knowledge-centre/pension-schemes/partnership-pension-account/, August 2024.

Sims, Sam. “What Happens When You Pay Shortage-Subject Teachers More Money? Simulating the Effects of Early-Career Salary Supplements on Teacher Supply in England.” London: The Gatsby Charitable Foundation, November 2017.

Teachers’ Pensions. “Valuation of Teachers’ Pensions.” Teachers’ Pensions. https://www.teacherspensions.co.uk/employers/employer-faqs/valuation.aspx, 2021.

Which? “Top up the Pots: Achieving Adequate Retirement Incomes with Automatic Enrolment.” Policy Report. London: Which?, May 2019.

Zuccollo, James. “Do Teachers Want Pension Flexibility?” Education Policy Institute, August 2024.

———. “The Workforce Challenges Facing an Incoming Government.” Education Policy Institute. https://epi.org.uk/publications-and-research/blog-the-workforce-challenges-facing-an-incoming-government/, June 2024.

Footnotes

James Zuccollo, “The Workforce Challenges Facing an Incoming Government,” Education Policy Institute (https://epi.org.uk/publications-and-research/blog-the-workforce-challenges-facing-an-incoming-government/, June 2024).↩︎

Dawson McLean, Jack Worth, and Andrew Smith, “Teacher Labour Market in England: Annual Report 2024” (NFER, 2024).↩︎

Department for Education, “Evidence to the STRB: 2025 Pay Award for Teachers and Leaders” (UK: Department for Education, December 2024).↩︎

Blessing Chiripanhura, “Public and Private Sector Earnings” (Office for National Statistics, September 2020).↩︎

National Audit Office, “Public Service Pensions,” Report -- {{Value}} for Money (London: National Audit Office, March 2021).↩︎

“Partnership Pension Account,” Civil Service Pension Scheme (https://www.civilservicepensionscheme.org.uk/knowledge-centre/pension-schemes/partnership-pension-account/, August 2024).↩︎

Department of Health and Social Care, “NHS Pension Scheme: Increased Flexibility,” GOV.UK (https://www.gov.uk/government/consultations/nhs-pension-scheme-increased-flexibility, September 2019).↩︎

Jon Coles, “Why We’re Reforming Our Pension Offer,” Schools Week, July 2024.↩︎

Lucas Cumiskey, “Unions Lobby Phillipson over United Learning Pension Plans,” July 2024.↩︎

James Zuccollo, “Do Teachers Want Pension Flexibility?” Education Policy Institute, August 2024.↩︎

Teachers’ Pensions, “Valuation of Teachers’ Pensions,” Teachers’ Pensions (https://www.teacherspensions.co.uk/employers/employer-faqs/valuation.aspx, 2021).↩︎

Neil Barton, “Latest Update – Independent Schools Leaving the Teachers’ Pension Scheme,” Broadstone, April 2021.↩︎

Dillon Fuchsman, Josh B. McGee, and Gema Zamarro, “Teachers’ Willingness To Pay For Retirement Benefits: A National Stated Preferences Experiment,” EdWorkingPapers.com (Annenberg Institute at Brown University, October 2020).↩︎

Andrew C. Johnston and Jonah Rockoff, “Pension Reform and Labor Supply,” EdWorkingPapers.com (Annenberg Institute at Brown University, May 2022).↩︎

Cory Koedel and Michael Podgursky, “Teacher Pension Systems, the Composition of the Teaching Workforce, and Teacher Quality. Working Paper 72.” National Center for Analysis of Longitudinal Data in Education Research, 2012.↩︎

Barbara Biasi, “Salaries, Pensions, and the Retention of Public-Sector Employees: Evidence from Wisconsin Teachers” (Working Paper, July 2024).↩︎

Peter Burge, Hui Lu, and William Phillips, “Understanding Teaching Retention: Using a Discrete Choice Experiment to Measure Teacher Retention in England,” February 2021.↩︎

Fuchsman, McGee, and Zamarro, “Teachers’ Willingness To Pay For Retirement Benefits”.↩︎

Zuccollo, “Do Teachers Want Pension Flexibility?”; Fuchsman, McGee, and Zamarro, “Teachers’ Willingness To Pay For Retirement Benefits”.↩︎

Chris Chapman and Elea McDonnell Feit, R For Marketing Research and Analytics, Use R! (Cham: Springer International Publishing, 2019), https://doi.org/10.1007/978-3-030-14316-9.↩︎

Jo Hutchinson et al., “Incentives to Recruit and Retain Teachers in Wales” (London: Education Policy Institute, November 2024); Sam Sims, “What Happens When You Pay Shortage-Subject Teachers More Money? Simulating the Effects of Early-Career Salary Supplements on Teacher Supply in England” (London: The Gatsby Charitable Foundation, November 2017).↩︎

Which?, “Top up the Pots: Achieving Adequate Retirement Incomes with Automatic Enrolment,” Policy Report (London: Which?, May 2019).↩︎